Building Your Emergency Fund: How Much You Need and Where to Keep It

Learn how to build an emergency fund from scratch. Free calculator with step-by-step guide. Covers how much to save (3-6 months), where to keep it (high-yield savings), and realistic timelines.

What would you do if your car broke down tomorrow and the repair cost $1,500? Or if you lost your job next month? For most people, these scenarios trigger immediate stress and worry about money.

You're not alone. About 70% of Americans couldn't cover a $1,000 emergency expense without going into debt or asking family for help. But it doesn't have to be this way.

An emergency fund is your financial safety net (cash set aside specifically for life's unexpected curveballs). This guide will show you exactly how much to save, where to keep it, and how to build it step by step, even if you're starting with just $25 a month.

Here's the good news: You don't need a huge income to build an emergency fund. You just need a plan, consistency, and the free tools we're building to help you every step of the way. We're here to make this easier, not harder.

(And yes, building an emergency fund is about as exciting as flossing your teeth. But just like flossing, everyone feels better when they actually do it.)

An emergency fund prevents you from going into debt when unexpected expenses hit. It's the difference between a stressful inconvenience and a financial crisis. Plus, knowing you have money set aside for emergencies brings real peace of mind. You can handle whatever life throws at you.

What is an Emergency Fund?

A savings account designated specifically for unexpected expenses like medical bills, car repairs, or job loss. Financial experts typically recommend saving 3 to 6 months' worth of essential living expenses. This money should be kept separate from your regular savings or investment accounts.

Think of your emergency fund as financial insurance. You hope you never need it, but you'll be incredibly grateful it's there when something goes wrong.

Here's what an emergency fund is NOT for:

- Vacations or travel

- Upgrading to the latest iPhone before your current one dies

- Holiday shopping

- Concert tickets or events

- Any planned or discretionary purchase

Your emergency fund is your first line of defense against debt. When you have cash set aside, you don't need to put unexpected expenses on a credit card or take out a payday loan. You can handle the emergency, pay for it in cash, and move on with your life.

How Much Should You Save?

The standard advice is to save 3 to 6 months of essential expenses. But what does that actually mean? Let's break it down.

First, "months of expenses" means your actual monthly spending on essentials (NOT your income). Calculate your monthly costs for:

- Rent or mortgage

- Utilities (electric, water, gas, internet)

- Groceries

- Insurance (health, car, home/renters)

- Transportation (car payment, gas, public transit)

- Minimum debt payments

- Other necessities

For example, if your essential monthly expenses total $3,000, multiply by 3 to 6:

- 3 months: $9,000

- 4 months: $12,000

- 6 months: $18,000

This can feel overwhelming. That's completely normal. Remember, you don't need to save this all at once. We'll show you how to build it gradually.

How Much Do YOU Need?

The right target depends on your personal situation. Here's how to think about it:

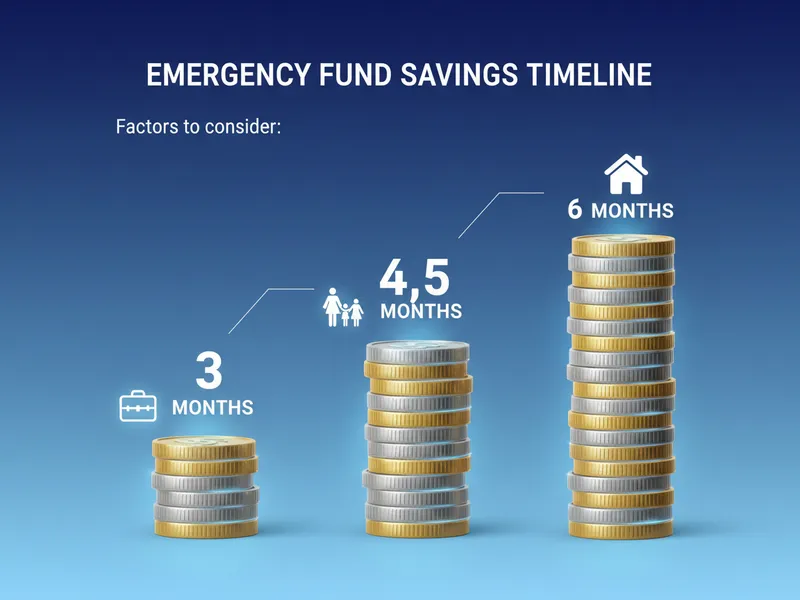

Aim for 6 months if you:

- Are self-employed or a freelancer (irregular income)

- Work in a volatile industry (tech layoffs, seasonal work)

- Are the sole income earner for your household

- Have health issues or dependents with special needs

- Own a home (more potential for expensive repairs)

Aim for 3 to 4 months if you:

- Have a stable job with steady income

- Are in a dual-income household

- Rent (landlord handles most repairs)

- Have good health and no dependents

- Work in a stable industry

Start with $1,000 if you:

- Are just beginning to build savings

- Are paying off high-interest debt

- Need a quick, achievable first goal

Most experts recommend 3 to 6 months of expenses, but the right amount depends on your job stability, health, and risk tolerance. Start with a mini goal of $1,000 to cover common emergencies, then build to 1 month of expenses, then 3 months, then 6 months. Small milestones keep you motivated and make the big goal feel achievable. You've got this.

Calculate how long it will take to build your emergency fund

→Real-World Example

Let's say your monthly essential expenses are $3,500 (rent, utilities, groceries, car payment, insurance, etc.). You decide to save $400 per month.

Your timeline:

- $1,000 emergency fund: 2.5 months

- 1 month of expenses ($3,500): 9 months

- 3 months of expenses ($10,500): 26 months

- 6 months of expenses ($21,000): 52 months (about 4 years)

Yes, building a full 6-month emergency fund takes time. That's completely normal, and honestly, that's okay. The important thing is to start now, even if it's small. At a 3.5% annual return in a high-yield savings account, you'll also earn interest along the way, which helps your money grow a bit faster.

Don't let the timeline discourage you. Every dollar you save today is a dollar you won't need to borrow tomorrow.

Where Should You Keep Your Emergency Fund?

Your emergency fund should be in a high-yield savings account at an FDIC-insured bank. As of early 2025, many high-yield savings accounts offer around 3.5% annual percentage yield (APY).

Here's why a high-yield savings account is perfect for emergency funds:

- FDIC insured: Your money is protected up to $250,000

- Liquid: You can access it within 1 to 2 business days

- Earns interest: 3.5% is much better than the 0.01% most regular savings accounts offer

- Safe: No risk of losing money like stocks or crypto

- No penalties: Unlike CDs, you won't pay a fee for early withdrawal

Don't invest your emergency fund in stocks, index funds, or cryptocurrency. The stock market is too volatile for money you might need next month. Imagine needing to withdraw during a market crash (you'd lock in losses). Don't keep it in a certificate of deposit (CD) with early withdrawal penalties. And definitely don't use a credit card as your "emergency fund" (that's just debt waiting to happen).

Why Not Just Keep It in Your Checking Account?

Two reasons: temptation and earnings. If your emergency fund sits in your checking account alongside your everyday spending money, it's too easy to accidentally (or intentionally) dip into it for non-emergencies. A separate savings account creates a helpful barrier.

Plus, checking accounts typically earn 0% interest. A high-yield savings account at 3.5% means you're actually making money while your emergency fund sits there safely.

Think of it like a spare tire. You keep it in the trunk, not in the back seat where you might sit on it. Same idea here.

- FDIC insured up to $250,000 (your money is protected)

- Liquid and accessible within 1 to 2 days when needed

- Earns around 3.5% interest (much better than checking)

- No market risk (your balance won't go down)

- No withdrawal penalties like CDs have

- Returns lower than stock market averages (but safety is the point)

- Interest may not keep pace during high inflation years

- Takes 1 to 2 days to transfer (not instant like checking)

Where to Open a High-Yield Savings Account

If you're looking for a high-yield savings account with no monthly fees and competitive rates, SoFi's checking and savings accounts* are worth considering. They offer:

- Competitive APY (around 3.5% as of early 2025)

- No monthly maintenance fees

- FDIC insured up to $2 million (through partner banks)

- Mobile app with budgeting tools built in

- Sign-up bonus for new members

The no-fee structure is especially important for emergency funds. You don't want monthly fees eating into your savings.

Disclosure: This is an affiliate link. If you sign up through this link, we may earn a small commission at no cost to you, and you'll receive a sign-up bonus. We only recommend products we genuinely believe will help you build your emergency fund.

How to Build Your Emergency Fund (Step by Step)

Building an emergency fund from scratch can feel overwhelming. We get it. That's why we're breaking it down into manageable steps. You don't have to do this perfectly. You just have to start.

Step 1: Calculate Your Monthly Essential Expenses

Write down everything you can't avoid paying each month:

- Housing (rent/mortgage)

- Utilities (electric, water, gas, internet, phone)

- Groceries

- Insurance (health, car, home/renters)

- Transportation (car payment, gas, maintenance)

- Minimum debt payments

Example: $2,800/month in essential expenses

Notice we're NOT including:

- Dining out or entertainment

- Subscriptions (Netflix, Spotify, gym)

- Shopping or hobbies

- Vacation savings

Your emergency fund covers basics only. You can always cut discretionary spending during an emergency.

If you're not sure where to start, don't worry. We're building more free tools to help you track and categorize your spending. For now, just do your best estimate.

Step 2: Set Your Initial Goal at $1,000

This is your mini emergency fund. It won't cover a job loss, but it WILL cover:

- Most car repairs ($500 to $800 on average)

- Many medical copays and deductibles

- Small home repairs (broken appliance, plumbing issue)

- Pet emergencies

Hitting $1,000 is achievable, motivating, and immediately useful. It's also a huge psychological win that builds momentum.

Step 3: Automate Your Savings

This is the most important step. Set up an automatic transfer from your checking account to your high-yield savings account on the same day you get paid.

Why this works: You're paying yourself first, before you have a chance to spend the money. Even if it's just $50 per paycheck, that's $100 to $200 per month, which gets you to $1,000 in 5 to 10 months.

Common automation strategies:

- Transfer a fixed amount: "$100 every payday"

- Transfer a percentage: "10% of every paycheck"

- Round-up apps: Automatically save the difference when you round purchases to the nearest dollar

Automation takes the decision-making out of it. You set it once and forget it. Your future self will thank you.

Step 4: Find Extra Money to Save

Look for ways to accelerate your savings:

- Cut one or two subscriptions ($10 to $30 per month)

- Brown bag your lunch twice a week instead of eating out ($50 to $100 per month)

- Put any windfalls toward your fund (tax refund, work bonus, birthday money)

- Sell stuff you don't use anymore

- Pick up a side gig (even $200 per month helps)

You don't need to do all of these. Pick one or two that feel doable. Small changes add up.

Treat your emergency fund contribution like a non-negotiable bill. You wouldn't skip your rent payment, right? Think of your emergency fund the same way. Every time you get a raise, increase your automatic transfer by 1%. You won't miss the money, and your emergency fund will grow faster. We're working on tools to help you track this automatically.

Step 5: Build to 1 Month of Expenses

Once you hit $1,000, keep going to your first full month of expenses. If your monthly essentials are $2,800, your next milestone is $2,800.

This level of savings protects you against:

- Short-term job loss (while you find another job)

- Bigger car or home repairs

- Multiple emergencies hitting at once

Step 6: Continue to 3 to 6 Months

This is your ultimate goal (full financial security). At 3 to 6 months of expenses saved, you can handle nearly anything life throws at you:

- Extended job loss

- Major medical expenses

- Unexpected move or relocation

- Multiple large emergencies

Yes, it takes time. But once you're there, the peace of mind is incredible. And remember, we're building free tools to help you track your progress and stay motivated along the way.

Common Emergency Fund Mistakes

Many people think "I can't afford to save much, so why bother?" But starting with $25 a month is infinitely better than $0. That's $300 a year, which becomes $1,500 in 5 years (plus interest). Small amounts compound over time. Start with what you can, even if it feels tiny. Progress beats perfection every single time.

Mistake #2: Using It for Non-Emergencies

A Black Friday sale is not an emergency. A vacation is not an emergency. Upgrading your phone is not an emergency.

Define what counts as an emergency BEFORE you need the money:

- Job loss or significant income reduction

- Medical emergency or unexpected health expenses

- Urgent home repair (broken furnace in winter, roof leak)

- Critical car repair needed for work

- Emergency family travel

If it's not urgent, unexpected, and necessary, it's not an emergency. Find another way to pay for it.

Mistake #3: Stopping Once You Hit Your Goal

Your emergency fund isn't "set it and forget it." When you use it (and you should use it when you have a real emergency), make rebuilding it your top priority. Pause extra debt payments or other savings goals temporarily until your emergency fund is back to its target level.

Think of it like a rechargeable battery. Use it when needed, then recharge it right away.

Mistake #4: Keeping It Too Accessible (or Too Hard to Access)

If your emergency fund is in your checking account, you'll accidentally spend it. But if it's locked in a CD with penalties, you won't use it when you should.

The sweet spot: A separate high-yield savings account at a different bank from your checking account. It takes 1 to 2 days to transfer (enough friction to prevent impulse spending), but it's still accessible when you truly need it.

When to Use Your Emergency Fund

Use It For:

- Job loss or reduced income (covers bills while you find new work)

- Major medical expenses (hospital bills, surgeries, serious illness)

- Urgent home repairs (broken furnace, water heater, roof leak, burst pipe)

- Critical car repairs (transmission, engine, anything needed to get to work)

- Emergency travel (family emergency requiring immediate travel)

Don't Use It For:

- Vacations or holiday travel

- Shopping (even if it's "on sale")

- Upgrading electronics or furniture

- Wedding or party expenses

- Anything you could plan and budget for

An unexpected, urgent, and necessary expense that can't be delayed or avoided. If you can see it coming or plan for it in advance, it's not an emergency (it's something you should budget for separately).

When in doubt, ask yourself: "Will not paying for this right now cause immediate harm or create a bigger problem?" If yes, it's probably an emergency. If no, find another way to pay for it.

Frequently Asked Questions

Should I save for an emergency fund or pay off debt first?

Both, but strategically. Here's the priority order most financial experts recommend:

- Save $1,000 for a mini emergency fund

- Pay off high-interest debt (credit cards, payday loans)

- Contribute enough to your 401(k) to get the full employer match

- Build your emergency fund to 3 to 6 months of expenses

- Pay off remaining debt while maintaining your emergency fund

The $1,000 mini fund prevents you from going back into debt when emergencies happen while you're paying off existing debt. Once high-interest debt is gone, focus fully on building your 3 to 6 month emergency fund.

What if I can't afford to save anything right now?

Start with whatever you can (even $10 or $25 a month). It's not about the amount, it's about building the habit and momentum.

Try this: Track every dollar you spend for one month. Most people find $25 to $50 they can redirect just by cutting one or two things they don't actually value. Maybe it's a subscription you forgot about, or eating out one less time per week.

Even $25 a month gets you to $1,000 in about 3.5 years. That's better than never reaching $1,000 at all. And hey, we're working on free budgeting tools to help you find that extra $25 faster.

Can I invest my emergency fund to earn higher returns?

No. Your emergency fund needs to be safe and liquid. The stock market averages 10% returns over decades, but it's volatile (it could be down 20% exactly when you need to withdraw money for an emergency).

High-yield savings accounts offering around 3.5% are perfect. You're earning reasonable interest without any risk of losing your principal. The safety and accessibility are worth more than the extra returns.

How long does it take to build an emergency fund?

It depends entirely on how much you can save each month. Here are some examples:

- $50 per month gets you to $1,000 in 20 months, $6,000 in 10 years

- $200 per month gets you to $1,000 in 5 months, $6,000 in 2.5 years

- $500 per month gets you to $1,000 in 2 months, $6,000 in 1 year

Use our free compound interest calculator to see your personalized timeline based on your monthly contribution and the interest rate your savings account earns. We're also building progress trackers to help you visualize your journey.

What if I have to use my emergency fund?

That's exactly what it's for! Don't feel guilty about using it when you have a genuine emergency.

Once you've used it, make rebuilding it your top financial priority. Temporarily pause extra debt payments beyond minimums, reduce discretionary spending, and redirect that money back to your emergency fund until it's replenished. Think of it as a cycle: build it, use it when needed, rebuild it, repeat.

Recommended Reading

Want to dive deeper into personal finance and building wealth? These books offer practical, actionable advice:

The Psychology of Money by Morgan Housel This bestseller explores the behavioral side of money management. Housel explains why building wealth is more about behavior and mindset than complex financial strategies. Perfect for understanding why emergency funds matter psychologically, not just financially.

Millionaire Mission by Brian Preston From the creators of The Money Guy Show, this book breaks down the exact steps to build wealth from scratch. It includes actionable frameworks for emergency funds, retirement planning, and smart investing. Practical, data-driven, and easy to follow.

Amazon Disclosure: These are Amazon affiliate links. If you purchase through these links, we may earn a small commission at no cost to you. We only recommend books we genuinely believe will help you on your financial journey.

Start Building Your Safety Net Today

Your emergency fund is the foundation of your financial security. It's what keeps unexpected expenses from turning into financial disasters. It's what lets you sleep at night knowing you can handle whatever comes your way.

The best time to start was yesterday. The second best time is today.

You don't need to save $10,000 overnight. Start with $25, $50, or $100 (whatever you can manage). Open a high-yield savings account this week, set up an automatic transfer, and let it grow.

Small, consistent contributions add up faster than you think. In a year, you could have $600, $1,200, or more. In three years, you could have a full 3-month emergency fund. Future you will be incredibly grateful that present you took this first step.

And remember, we're here to help. We're building free tools (calculators, progress trackers, budgeting helpers) to make this easier every step of the way. No ads, no account required, just straightforward help when you need it.

See how your emergency fund will grow with our free compound interest calculator

→You don't need to be perfect. You just need to start. Even if you can only save $10 this month, that's $10 more than you had before. Progress, not perfection.

You've got this. 💪